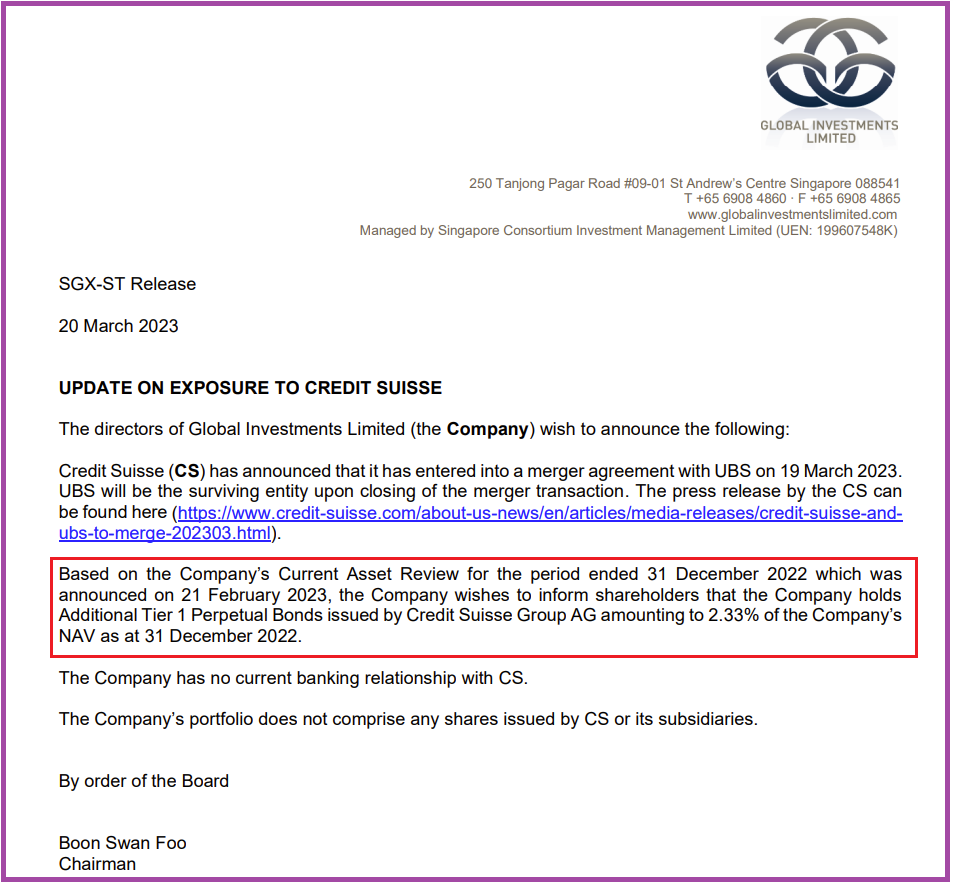

I thought that it is rather interesting to see marketing and mass communication techniques being employed into the SGX announcement by the management of Global Investment Limited ("GIL") to confirm that they have taken a hit in their CoCo with Credit Suisse and then express it in a nonchalant manner since it is only a "mere 2.33%" impact on its Net Asset Value of S$0.1682 as at 31 December 2023. The announcement has cleverly avoided mention of a full write-down by only inserting a URL for shareholders to read for themselves the other announcement coming out from Credit Suisse as well as astutely avoiding the quantification of the absolute quantum that is now worthless by only referencing to 2.33% of net assets.

1.Quantification of absolute amount lost in the Credit Suisse banking crisis- S$6.08Mil

|

| SGX announcement by GIL |

|

| Source: https://www.credit-suisse.com/about-us-news/en/articles/media-releases/credit-suisse-and-ubs-to-merge-202303.html |

The financial impact of the CoCos that the Swiss government has announced as a full write-down amounted to S$6.08 Million. This is actually an extremely high amount that is nearly half of the annual dividends income and interest income received by the GIL from its investments.

|

| Total Revenue from main investments of GIL |

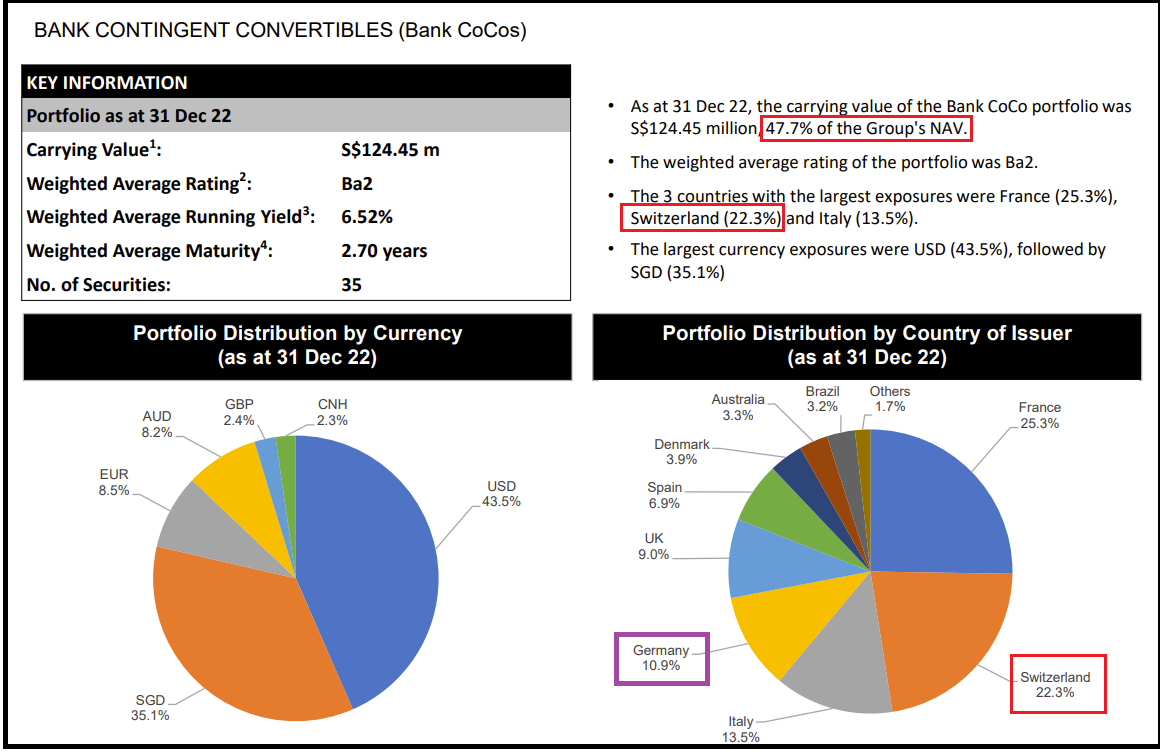

The worst aspect is that the banking crisis continues to spread with Deutsch bank, one of Europe's largest bank, also appearing to be in trouble from a lack of confidence- GIL has 10% exposure to Germany out of its total S$124.45 Million in bank CoCos.

|

| Another 10% potential exposure in CoCos coming up from Germany bank in trouble |

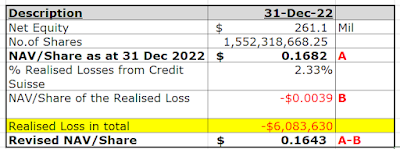

2. Net Asset Value after taking out Credit Suisse CoCos exposure

Parting thoughts

As at 24 March 2023, GIL is languishing at S$0.105 per share which is one of the lowest ever over the past 5 years. Tier 1 banking capital has become extremely risky in the prevalent market conditions and 47% of its net asset are stuck in CoCos. Personally, I am staying away from GIL for now until the banking crisis stabilized.

Please also see my previous post:"Global Investment Limited In Crisis Mode- 48% of Its Net Assets Are In Bank Contingent Convertibles (CoCos)."

Hi,

ReplyDeleteFirst, we should not look at only the absolute amount, but rather the impact on the fund. 2.33% impact is managable, since Global Investment Limited do not have debt. There is no risk of forced selling to pay down debt. There is also no risk of selling due to massive fund redemption since its a closed end fund, unlike open ended ones.

Second, we should not compare the write-down with the dividends/interest income received. Obviously, the dividends/interest income received will be impacted by the write-down, but not to the extent of S$6.08 million. One should only deduct income from those CoCos that had been wrote-off.

Thirdly, if you look at their annual report and their disclosed top 10 holdings, most likely their major exposure to Germany is via Commerzbank CoCos. Even if there is exposure to Deutsche Bank CoCos, it is not likely to be all the 10.9%. And since Bank CoCos is 47% allocation for the fund, it is also likely that Deutsche Bank CoCos exposure will be less than 3% of the NAV.

Finally, we should not use 31 December 2022 asset allocation information and then assume that Bank CoCos allocation stays at 47% currently. Global Investment Limited is an actively managed fund, and they might have reduced their exposure to Bank CoCos since then.

Hi ghchua Sir, thanks for dropping by. Wow, it is an honour indeed to have the great ghchua dropping by and sharing thoughts. Ok, now back to your comments. First and foremost, I did not say that GIL will collapse from "debt". Also, everybody's own investment philosophy is different and my blog posts are mainly for my own documentation. I do not have the power to talk down the market price neither am I responsible for its current decline in share price especially over the past week in the circumstances as it is.

ReplyDelete1. I disagree with you that one should only look at the 2.33% solely. Sorry, for me as an investor, I need to know the quantum. Also, these are "realised losses" and no longer fair value up and down. I will explain this further in point 2 below in response to your thoughts that comparing absolute quantum to the dividends and interest income is irrelevant;

2. Write down of S$6Mil in this case I will compare it to its annual dividend and interest income. Why? Simply for me, GIL is an income play (this may differ for you or others). It means basically, half of the usual recurring cashflow generated per year is gone as it needs to cover for the realised loss in capital to bring it up to the original level. Again this is a "realised" loss in capital and not the fair value loss that you can ignore and just wait to collect the interest coupon from the CoCos. Without knowing the absolute quantum, how do you also have a more transparent mental computation/forecast on the interest that will be lost from those coupons?

3. You seems to be leaning towards the camp that there will be very limited exposure to the current banking contagion from USA and Europe. If so, with due respect, you can buy more of GIL. But personally I am staying away for now. Its price has dropped from S$01.50 range to the current S$0.105 range over the past one year. In addition, I trust that you understand that GIL is not like other unit trust where the monthly traded price is equivalent to its NAV per share. It has always traded bellow its NAV;

4. This is the strangest part that I ever seen that one should not use 31 December 2022 asset allocation information. If not to use it, let's only make investment decision every half yearly only when there is a latest update or quarterly when a company released its financial information/asset allocation. In addition, if you think that GIL has already substantially reduced their CoCos, then you do realise that all the fair value losses previously reported would have became "realised" losses straight-away right?

Last but not least, whether GIL got reduce their exposure to Bank CoCos is a bit irrelevant at this juncture because they are in trouble either way-maintaining will means high exposure to the slowly unveiling of banking crisis while winding down will mean game over as unrealised losses became immediate realised losses.

(Note: By the way, I am currently still vested,1 share, in GIL).

HI Blade Knight,

ReplyDeleteThanks for sharing your thoughts. So, you don't think that GIL will "collapse" from debt. It is good to know, because you said that you are staying away from GIL now. Indeed, besides zero debt, they have around S$51m cash as at 31 December 2022. Maybe I try to response again to some of your additional comments here.

1. 2.33% is a write-off. I think we should look at realized and unrealized together as losses because they both hit NAV. As an investor, what I am trying to do is to buy GIL at a decent discount from NAV.

2. Its not really correct to compare it this way. Allow me to explain why. First, GIL pays dividends from dividend/interest income received so that it will not hit retained earnings badly when they have unrealized losses. It also do not really pay dividends out from unrealized gains for the past few years. There is no need to cover those realized losses to continue paying dividends, as long as the retained earnings is more than that. As at 31 December 2022, GIL had retained earnings of S$14.66m. I can also say that since they have S$51m cash, they have to put them back to use immediately to generate more income to make up for the lost cash flow. By the way, S$51m cash is around 20% of their NAV, enough to cover 2.33% cash flow lost from write-off dividends by investing.

3. I do not have a view on the markets or banking contagion. Basically, as an investor, my aim is to buy companies at a discount. The more the discount, the more I will be interested in. Of course, I will look at individual companies closely and see if the discount is justified based on my understanding of them. Yes, I do know that GIL normally trades at around 30% from its NAV. Just for your info, I bought GIL mainly for NAV discount, and not so much on income. This is not the first time you will see this kind of volatility in GIL share price and it will not be the last. I remembered they also experienced that in late 2018/early 2019 due to Deutsche Bank issues.

4. What I am trying to say is to use 31 December 2022 asset allocation information as a guide. When you are investing in a fund, what you are doing actually is investing in the manager running it. Yes, you can use those information as a guide, but what is also important is the track record of the manager. Did they deliver consistent returns over the years? Are they experienced managers running funds and dealing with crisis? Can they recover from this crisis? To me, that is more important than looking at realized/unrealized losses/gains. And of course, the decision to buy/sell will be made based on how much is the trading price is at a discount from NAV.

Thank you ghchua Sir for clarifying and sharing how you look at GIL from your perspective...appreciate! I am staying away from GIL now is because I do not want to take on too much risk with the run on banks recently and the price and dividend payout may drop further....but saying that, if value over risk becomes attractive again, I will start to re-enter back into a bigger position.

DeleteI am still very much an income focused investor and more concern with sustainable dividends payout regularly. GIL missed out one dividend payout last year (1 instead of 2) due to market conditions and it wanted to preserve cash for investments. The current write-offs increase the probability of lesser payout again if its management choose to preserve cash for re-investment to build back its portfolio.

Over the years, my own personal view (may differ from many such as yourself) is that GIL has limited success, such as various share buybacks, to push up its market price to its rightful NAV. I don't mind to wait, but there must be a good dividend stream to compensate for the waiting.

Hi Blade Knight,

DeleteWith regards to that dividend, they have declared 0.4c interim and 0.4c final dividends this time round with their FY22 result. So, they didn't miss out on that dividend last year. It is just they are adopting a wait and see attitude due to their unrealized losses in 1HFY22 and have decided to defer the dividend decision to 2HFY22 result announcement. So, no change in dividend payout for FY22.

I agree with you that GIL share buybacks has limited success in bridging the gap between market price and NAV. This is because they had a scrip dividend scheme in place and they will almost always issue those shares bought back (at a discount) to shareholders again. I think I would have to engage the company more on their thoughts on this.

My feel is that GIL takes the dividend payouts seriously and will not unnecessary cut them. However, what we are encountering now is a crisis, so I do agree with you that there might be a chance that dividend payouts will be reduced. But with 20% cash hanging around, no debt and a scrip dividend scheme in place, I am quite comfortable that they will be able to tide through this round.