United Hampshire US REIT ("UHREIT") announced another set of stellar half year results. Its Gross Rental increased +13.3% while Net Property Income increased +14% relative to its prior 1st Half FY2022. It has also successfully improved committed occupancy for its groceries and necessities properties to a record high of 97.9% with new and renewal leases totalling 331K sqft being signed in the 1st half of FY2023. At the price of US$0.42 per unit as at 11 August 2023 and a distribution declaration of 2.65cents per unit, UHREIT is effectively giving out an annualised distribution yield of 12.86% and this is notwithstanding an amount of US$1.5Mil being retained by its management for asset enhancement initiatives (the distribution yield would have been even higher at 13.86% if all of it are marked for payout). Congrats to all fellow current unit-holders who have been taking market risk to hold on to this US REIT!

(Note: I have started my own You-Tube Channel and has uploaded a video on UHREIT there- please click here to follow & subscribe.)

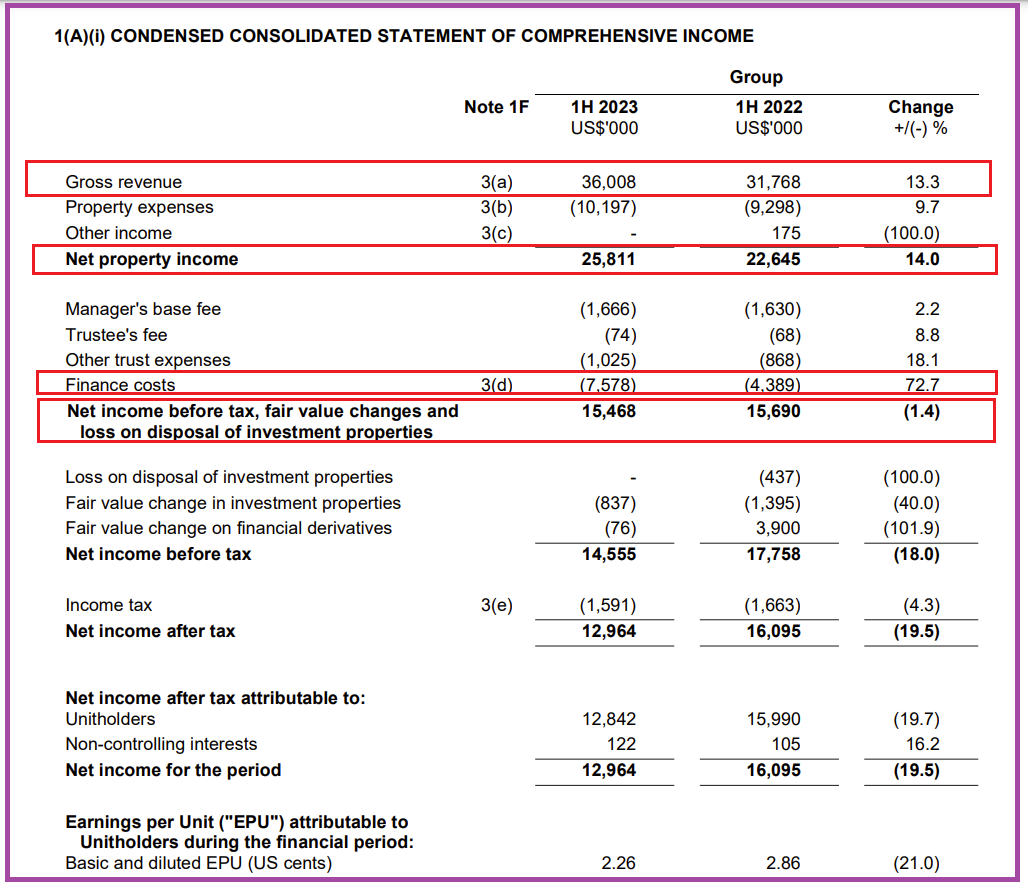

1. Quick Review of Financial Results for 1st Half 2023.

As aforesaid mentioned, the net property income has increased by 14%. However, the finance cost has went up by a whopping 72.7% which thus dragged down the overall net income before tax and fair value changes by -1.4%.

One point to note here is that for "Fair Value changes to investment properties or financial derivatives", these have no effect on the cashflow and distribution payout unless they are realised.

From the financial statements, there are actually 2 key risks that one should take note of and which I will elaborate further in the final portion on "Parting Thoughts" section later on.

2. Debt Profile Status of UHREIT

UHREIT has no major refinancing exercise coming up until November 2026. For 2024, there is a small tranche of US$21.1Mil of mortgage loan maturing only. Moreover, 80.9% of its debt are fixed interest at a weighted rate of 3.57%.

Aggregate leverage is at 42% which personally to me is on the high side- Please see UHREIT planned disposal of Big Pine Centre in section 3 below to repay part of its debt to bring down this ratio.

3. Planned disposal of Big Pine Centre at 3.7% Premium to Valuation

As part of its proactive portfolio and asset management strategy, the Manager has entered into an agreement to divest Big Pine Center, Florida, for a sale consideration of US$9.9 million. The consideration represents a 3.7% premium over the 31 December 2022 appraised value of US$9.5 million, and 7.7% premium over the purchase price of US$9.2 million.

Assuming the net proceeds are used to repay debt, UHREIT’s proforma gearing is expected to be reduced by 0.8%.

4. Million Dollar Question On UHREIT's Investment Properties Outlook- Will It Go Down the Road Of Manulife US Office REIT or Prime US Office REIT?

Interestingly, the Green Street Property Price index indicates that the remote work from home arrangement post COVID pandemic which severely affects US Office Commercial properties actually benefitted the Strip Centre sector which is the key properties held by UHREIT. Apparently, workers working from home increased the demand for the goods and services offered in Strip Centres.

From June 2020 to June 2023, the valuation of Stripe Centre increased 19%.

Similarly, Self-Storage properties (this is also one of the type of commercial property held by UHREIT but to a lesser extent) valuation went up by 58% over the past 3 years.

Parting Thoughts

The 2 key risks faced by local unit-holders of UHREIT are (i) forex risk arising from weakening USD due to wide-spread money printing by the US Fed and (ii) the high aggregate leverage ratio of 42% which makes is susceptible to breaches of bank loan covenants that automatically lead to loan default should there be structural headwinds in demand or higher interest rates hikes in the event that the inflationary monster comes back.

In addition, the structural setup of UHREIT seems to be eerily similar to Manulife US REIT which leads to a further question on whether rights issue to all unit-holders- as a last resort to raise funds- is actually feasible in the event of a debt crisis. According to Manulife US REIT, this rescue option cannot work as each unit-holder can only hold up to 9.8% of units in such a setup and the sponsor are thus unable to step in. This render having a "reputable and financially strong" sponsor as good as useless. I will probably be sending out queries to the management/public relation team of UHREIT to find out more.

US law is cumbersome. If cannot do Rights Issue, then what option is left?

ReplyDeleteHi Henry, how have you been?Thks for dropping by. With regard to this question, I am not sure too. Manulife US REIT Sponsor and their PR team seems to frown upon on rights issue and saying that it cannot be done due to the 9.8% max ceiling for a unit-holder. I will be dropping UH REIT a query to seek their clarification if we end up in a similar dooms day scenario over the debt ratio in future (touchwood).

DeleteHI BK

DeleteAlways enjoy reading your short and sharp posting. Do share in your blog when you get a reply from UH Reit.

Hi Henry, please see the update in my post on 22nd Aug 2023. https://dividendpassiveincome.blogspot.com/2023/08/updates-on-united-hampshire-us-reit-and.html

DeleteHi Blade Knight

ReplyDeleteI enjoyed reading all your posts. N like u , I am also vested in this UHREIT whose price is depressed despite it posting consistently good dpu results. With regard to the parting thoughts, u mentioned that UHREIT is eerily similar to Manulife in terms of structural setup. May I know y is this so? As Manu is in office reits while UHREIT is in grocery and self storage. One of the main reason for Manu's deterioration is due to wfh and remote workers but this instead boosted UHREIT in Stripe center. Are to referring to when workers return to work and this will affect UHREIT? But i note that Stripe center is just a portion of UHREIT whilst the grocery portion is the main revenue which is recession proof. If its recession proof, why should it lead to a debt crisis? Anyway, I note that the management is trying to bring down the leverage and kudos to that. Hopefully the share price will react upwards.

Hi Ju, good day to you. Thanks for dropping by. In terms of structural setup, I was referring to the tax structural setup to bring back the profits to SGX based unit-holders for SREITs with US properties without incurring withholding tax from Uncle Sam. Apparently, it may not just be a US withholding tax issue plus also a statutory collapse of the current companies setup structure if the shareholding cross 9.8%.

DeleteFor rights issue, not all Unit-holders will want to take part during crunch time and normally the sponsor will mop up any excess unsubscribed rights. But in this case, they will exceed their percentage of unit holding after the exercise and lead to a collapse of the organizational structure cleared by their professionals and govt authorities. Hence the rights issue which is a normal last resort to save the REIT becomes an untenable option apparently.

Hi Blade Knight

DeleteThanks for checking with the UHREIT. In the meantime, lets have faith in the business and the management. In such times of high interest rate hike, the business had proven to be resilient through its stellar results while several reits listed in sgx be it local or overseas have seen their dpu declined of late due to the rate hikes. We should be cheering on possible rate hike pause and cuts which is in the horizon. In the instance of turbulent times, a good performer can get better when bad times passed.

Hi Blade Knight

DeleteI just saw that United Ham is having a dialogue session with shareholders. Fyi.

https://adragonhoard.blogspot.com/2023/08/icymi-united-hampshire-us-reit-dialogue.html

Thanks Ju for the link. Have registered for the SIAS UHREIT dialogue. Hope that I do not have to OT that day and can attend. Last weekend I have dropped a list of queries on the 9.8% structure and rights issue to UHREIT investor relation but no sound no picture from them at all via email.

DeleteHi Ju, please see the update in my post on 22nd Aug 2023. https://dividendpassiveincome.blogspot.com/2023/08/updates-on-united-hampshire-us-reit-and.html

Delete