Lendlease REIT ("LREIT") unit price has been a disaster for over the past 1 year. From S$0.810 per unit to the current S$0.56 per unit, this is a <-31%> plunge in its market price in a mere 12 months. With a half year distribution of S$0.022453 annualized, this implied an 8% distribution yield. While I would love to add on to LREIT at its current weak unit pricing, there are a few worrying points that is making me hesitate to do any further accumulation. Let me elaborate further below:

1. Rights Issue Maybe On The Table Due to Further Acquisition of Parkway Parade LREIT has recently purchased a 10% stakes in Parkway Parade Shopping Mall. A rights issue maybe on the way for it to acquire more stakes or to takeover the remaining stakes. If the price of LREIT continue to remain in doldrums for some time and LREIT’s management called for a rights issue, the rights issue price is obviously going to end up 5% to 10% lower than its recent trading price per unit. In short, its unit price performance might worsen even more.

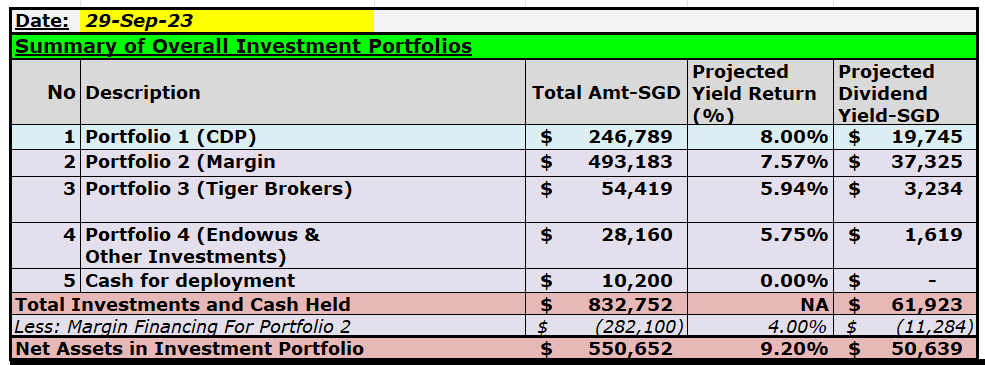

2. LREIT Already Make Up A Substantial Part of One’s Portfolio

LREIT is currently making up 8% of my overall combined portfolios. For those folks who are in the same predicament as mine, accumulating more units in LREIT may mean even higher concentration risk. For example, black swan event like COVID hit retail malls extremely hard.

In addition, as alluded to Pt 1, once there is a rights issue, existing unit-holders will need to take part to avoid dilution in their holdings.

3. LREIT Gearing Ratio Exceeded 40%

LREIT’s gearing ratio has hit an uncomfortable 40.6% as at 30 June 2023. In the event that the World entered into a global recession, this may lead to sharp drop in property valuation and in turn leads to breaches in MAS regulatory requirement or banking covenants.

Parting Thoughts

Personally, the S$0.56 per unit pricing as at 18 September 2023 and 8% distribution yield seems rather attractive coupled with the upcoming completion of the redevelopment of Grange Road open air car park into a multi functional event facility as well as having a long list of potential M&A pipelines from its Sponsor. Nevertheless, as aforesaid mentioned, I will probably re-deploy excess funds on hands into Endowus fixed income funds instead to ensure sufficient diversification.