With the invasion of Ukraine by Russia, United Hampshire US REIT ("UH REIT") was not spared the carnage on world-wide stock markets with the already low trading price being further hammered till US$0.61 per unit as at 25 February 2022 (Friday) closing despite the relatively good results just being announced. Given the total DPU for the full FY2021 is US$0.061, this means an extremely attractive distribution yield of exactly +10.0% per annum, not withstanding the fact that the latest acquired properties contribution only came into effect on 14th October 2021. This also means that for FY2022, UH REIT stands to enjoy another upside of 9.5 months of additional rental contribution coming from Penrose Plaza Philadelphia and Colonial Square Shopping Centre Virginia. I will also attempt to elaborate a bit later on why the current ongoing war in Ukraine actually benefits REITs based in US.

1. 2nd half 2021 results highlight

|

| Financial highlights comparison to forecast and historical results |

|

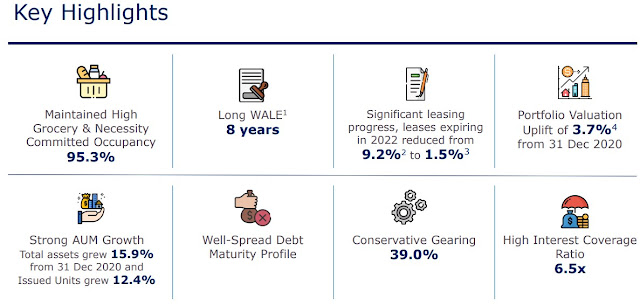

| Operating metrics appear healthy |

As we can see, UH REIT financial results remain well within expectation. Its performance has also improved a lot if compared to historical 2nd half numbers. Operating metrics such as leases expiring in 2022 has been reduced from 9.2% (as at 31 Dec 2020 )t o only 1.5% (as at 31 Dec 2021) with good work by their business development team on renewal. In addition, its WALE is relatively high at 7.9 years which gives much stability to recurring rental income.

2. Sales of self storage facilities and income support complaint by retail investors

I am glad that UH REIT has entered into a conditional sales of their self storage properties Elizabeth and Perth Amboy for a sales consideration of US$49 Mil (before transaction costs). Taking into account the purchase price of US$43.4Mil inclusive of income top-ups, this represented a +12.9% sales premium.

Whenever UHREIT is mentioned, there will be retail investors bringing up the topic of income support of these facilities and associated grievances about the "artificial" rental income. It is thus good to realise the associated profits with these self-storage to lock the profits and then recycle the capital.

3. Effect of ongoing war in Ukraine by Russia on US.

The ultimate winner of the current Ukraine war will be USA. US will be selling more weapons to its European allies in view of the "belligerent" Russia Federation. The shale oil industry in US will also benefit from the upcoming sharp increase in oil & gas prices not to mention the possibility of exporting oil to European allies should Russia stop the shipment of oil & gas to Europe in view of the SWIFT ban being imposed on Russian banks.

During world war 1, the US economy was in recession. But a 44 month economic boom ensued from 1914 to 1918 as Europeans begin purchasing US goods for the war. Such is the economic reality of war. So, I expect the economy of US to be doing very well in the near future albeit the ongoing smaller scale war. This should continue to support grocery and necessity properties from the trickle down effect.

4. Main key risks for investors of UH REIT

Retail investors need to also consider risk factors associated with holding on to UH REIT and not get overly excited with the incredulous 10% distribution yield annually.

Retail investors need to also consider risk factors associated with holding on to UH REIT and not get overly excited with the incredulous 10% distribution yield annually.

a. Rental rates cannot catch up with the rapid inflation.

While there are rental escalation clauses, the rate of inflation spike may be a lot higher and faster than the allowed rental escalation.

b. US withholding tax changes.

We need to be careful of US tax authority IRS changes in tax rules. Currently, the US REITs listed on SGX are using special vehicles in US and sending back dividends to Singapore via a capital distribution model in order to get past the withholding tax requirement (tax shield). Note that US authorities may pass legislation to change this and having withholding tax being levied will reduce a substantial part of the dividends derived from US properties.

For those interested on the technicality of the US tax shield employed by US REITs listed on SGX, I have previously done up a short write-up on the background and origin of "capital distribution" of US REITs in my Manulife US REIT posting here.

c. Low trading volume on SGX.

Personally, I find the daily trading volume of UH REIT to be on the low side. It is not very liquid. If one is in urgent need of cash and needs to sell, you may have to drop the price a lot in order to liquidate your holdings fast.

d. Loss of economic moat due to e-commerce

What if online fulfilment became cheap and efficient enough to deliver groceries directly from vendor's warehouse to the consumer at their own home? Will renting physical property still be necessary? Retail investors will need to keep a close watch on the market trend and sell immediately if this model of ownership is no longer relevant. The issue of being geographically far from the actual location of the properties to have adequate and timely visibility is another physical challenge in monitoring.

Parting thoughts on UH REIT being a cash cow with super attractive yield of 10%

Notwithstanding the key risks as discussed above, FY2022 looks set to be another good year for UH REIT with the upcoming sales of the self-storage properties at a premium of 12.9% to cost as well as the additional rental contribution from Penrose Plaza and Colonial Square Shopping Centre. If UH REIT can re-deploy the sales proceeds fast enough for additional yield accretive acquisition towards the end of FY2022, this could be another price catalyst. I do hope that the sales of the self-storage properties would at least unlock part of the hidden value trapped within the current US$0.61 per unit which is grossly undervaluing the REIT from its IPO price of US$0.80 per unit in March 2020. UH REIT has so far produced a good track record of its resilient earnings throughout this COVID pandemic since IPO.

would the bullwhip effect from logistics cause further impairment ? And also in view of the upcoming recession/stagflation ?

ReplyDelete