Recently, S-REITs unit price collapsed along with most of the world wide stock-markets. The once rising star of data centres focused REITs, Keppel DC REIT, plunged to a record 52 weeks low of S$2.16 per unit as at 28 January 2022 (Friday) . The speed of the devastating plunge in the last 2 weeks shell-shocked many retail investors as just 12 months ago, the price of Keppel DC REIT was at its 52 week high of S$3.040 per unit in the midst of the COVID pandemic and its meteoric rise looked unstoppable. So what has happened to this infallible bright star, that some investors proclaim is a REIT with the potential of a growth stock with numerous upcoming M&A opportunities yearly, to cause it to fall into the abyss? Should investors start dumping all units in Keppel DC REIT in view that prices seems to be plunging dramatically every day?

1. Upcoming macro-economic background changes- sky high inflation in US.

The Federal Reserve has left interest rates and a key bond-buying taper plan unchanged on Wednesday 26th Jan 2022 but nevertheless, it has given a clear signal that the period of easy-money policies is coming to an end as inflation soars to a 40-year high and joblessness comes close to a half-century low. The current Federal Reserve fund rate is at 0% to 0.25%. The forecast by Analysts projected a 3-4 impending hikes for the Federal Reserve Fund rate of approximately 0.75% to 1.00% for FY2022 and 1.75% to 2.00% for FY2023. This will in turn push up world-wide interest rates.

The severe decline in prices of Keppel DC REIT as well as other S-REIT is thus attributable to not just expected higher cost of borrowings but most importantly, if risk-free bond rate starts to go up, the expected returns from holding REITs by all investors will need to increase on top of current yield. To find the short term equilibrium pricing, ceteris paribus, the price of a REIT thus has to drop in order to adequately compensate investors for holding on. I expect the pricing volatility and the declining trend to continue for the next 2-3 months at least.

2. What is the impact on REIT pricing and when will the price collapse bottom out?

Let's use Keppel DC REIT distribution per unit as an example. Recent distribution per unit for FY2021 is 9.851 cents. Its price on average over the last 6mths is around S$2.50 per unit.

Let's use Keppel DC REIT distribution per unit as an example. Recent distribution per unit for FY2021 is 9.851 cents. Its price on average over the last 6mths is around S$2.50 per unit.

This gives rise to a distribution yield of 4.1%. From a high level perspective, if risk free interest rate is expected to increase by an additional +0.75% to +1.0 % in the near term, one would expect a yield of 4.85% to 5.1% after the adjusted new risk free treasury rate.

This will mean a pricing range of S$1.89 to S$2.04 per unit eventually.

However, I think that such simplistic basis and current panic mode is way too pessimistic on fair value assessment. I will also use another full data Centre focused REIT, Digital Core as comparative benchmarking to project my own assessment of a fair market value for a sanity check. Please see Pt 3 below.

3. Proxy bench marking to other Data Centre REIT- Digital Core REIT.

The IPO price of Digital Core REIT is US$0.88 per unit. Taking into account many investors expecting the yield of 5.26% from its 2nd year onwards and the strong performance post IPO price of US$1.15 per unit, this will imply an expected yield of 4.03% for data centre assets despite the proclamation by the US Federal Reserve to increase interest rates.

Personally, I view Keppel DC REIT to be vastly better than Digital Core REIT given that the former has a geographically wider diversification of its data centres relative to the latter. In addition, the sponsor of Keppel DC REIT is Keppel Corp with a strong pipeline of data centre in developments as well as the financial might of Temasek rallying behind them.

Using 4.03% yield as proxy, Keppel DC REIT's fair valuation pricing should be around S$2.44 per unit. As at 25 Jan 2022, it is interesting to note that CGS-CIMB analysts have a target price of S$2.70 for Keppel DC REIT.

Parting thoughts

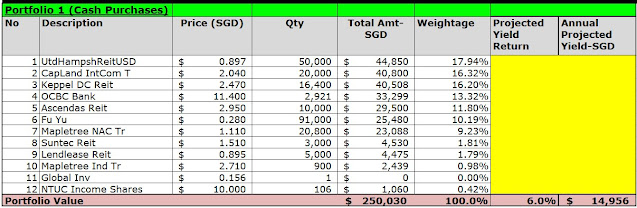

Given the strong demand for data centres worldwide and the potential for acquiring yield-accretive assets in the pipelines for Keppel DC REIT, I think that the current interest rate hike issue has been overblown and that many investors have been beating it down way below its fair value at the current low price of S$2.16 per unit. For me personally, I have taken the opportunity in this recent sell down to increase my holdings in Keppel DC REIT. It has climbed to the top 3 investment holdings in my overall portfolio.