I am not sure why many analysts were very pleased with the latest Q4 2022 results released by Alibaba (despite it depicting a huge loss worst than the prior Q4 quarter of 2021) which they think is much better than their expectation. The US and HK stock exchanges for Alibaba also went up between 12%-15%. For me personally, I am holding a contrarian view for the near term as despite the 9% growth in revenue for Q4 2022 year on year, Income from Operations has actually fallen off the cliff after normalising for reversal of share-based compensation expenses of RMB13,046 Million in Q4 2022-meaning a razor thin profit from Operations of only RMB 3,671 Million for Q4 2022. This also means that the Net Loss for Q4 2022 is approximately <RMB 31,403 Million> after normalisation.

1. Loss of RMB18.4 billon dollars on RMB 204 billion dollars of revenue for Q4 2022 results

The bad news here is that the pressure on gross profit margin from the anti-monopoly measures forced down on Alibaba seems to have squeezed the life out of the e-commerce giant. In FY2021, its Q4 Loss from Operations included a RMB 18 Billion (US$2.7 Billion) Anti-monopoly. Hence the actual decline for the same Q4 year on year is a whopping RMB 31.4 Billion decline.

The other complication here with regard to earnings visibility is the impact of COVID-19 disruption to Alibaba operations. As China gradually open up its economy, the million dollar question here is whether the number of transactions generated from e-commerce spending by consumers during lockdowns will decline drastically as some consumers head back to traditional purchases. Hence based on its current Q4 results, the results are murky and personally, I am unable to tell with more certainty on the general trending for Alibaba's future performance.

2. Silver lining in the dark cloud

As mentioned earlier, the good news is that Alibaba continued to grow their revenue by 9% based on Q4 year on year. This is a rather impressive feat given the multi-faceted challenges in the regulatory environment and also covid 19 lockdown disruption to the supply chain.

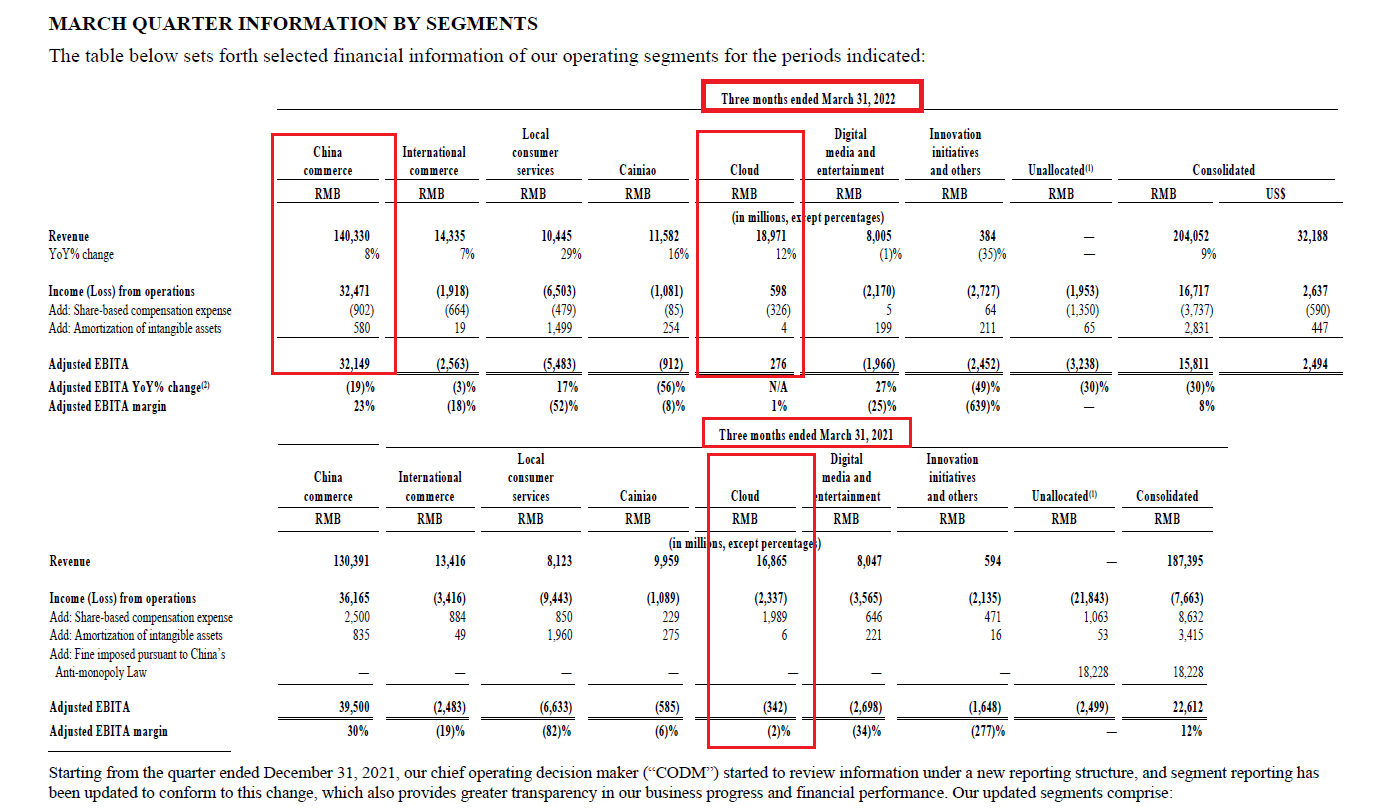

In addition, the adjusted EBITA for Cloud segment of Alibaba Group shows a profit RMB276million for Q4 2022 instead of a loss of RMB342million for previous Q4 2021, largely attributable to the realisation of economies of scale. This is a rather good sign as besides China e-commerce segment, the Cloud segment seems to have grown in size and generating a positive EBITA despite the pulling out of cloud services by state-own companies (as ordered by regulators over cybersecurity concerns of Alibaba and Tencent in Dec 2021).

Last but not least, its international e-commerce business fronted by Lazada continues to grow rapidly. Although the planned IPO for Lazada has been halted for now due to less than ideal valuation, there will be upsides to Alibaba group from its listing once the market conditions improves.

Parting thoughts

Overall, despite the headwinds from the competitive e-commerce landscape and uncertain times, Alibaba continued to invest into strengthening its eco-system to generate revenue growth and has taken drastic measures such as laying off (around 15%) of its workforce to optimize its operating cost structure in order to enhance overall returns to shareholders. I will continue to hold my small stake in Alibaba while awaiting greater clarity in its next quarter earning release.