I decided to pen this post after having a recent chit chat with my old friend from University as well as a "war buddy" during our younger days doing battles with auditing field assignments together (day and night) for almost 2 years. Well, yup, I mentioned "our younger days" as we are now old men with lower energy (岁月不饶人) and have since moved on to our respective jobs in the commercial sector. Anyway, we were talking about the latest topic in the market, that is, the bloodbath in China Tech and Education stocks due to the regulatory Big Brother coming in to smash and end the party. From there we also touched on something contentious, that is, the investing philosophies of my old friend and I are as different as day and night which I will elaborate more below.

1. Invest and hold for long term or hit and run?

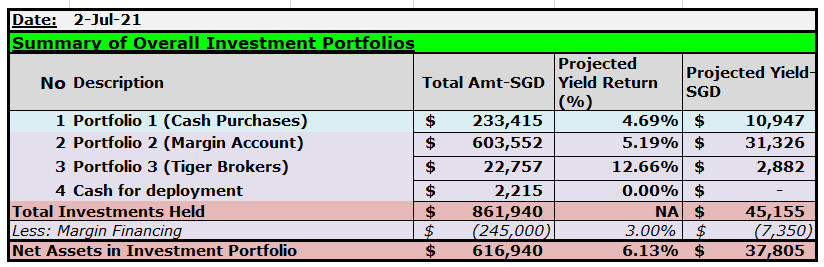

Those who have come across my blog will know that I am an overall income focused long term investor. The reason why I am so fixated on building up a passive income sum (instead of embarking on a capital growth investment strategy for retirement) is that I do not think job security exist in the current job market right now- anyone can be retrenched anytime (even if you work hard) especially if you unknowingly say the wrong words and offended your Boss...haha. So, most of my investments are into higher dividend paying REITs and stocks on SGX which helped generate a side income.

My old buddy on the other hand thinks that it is silly to be investing long term in the market as one would be subject to market ups and downs like the recent pandemic recession last year which lead to market crashing in March 2020. For him, investing is about being a sniper by finding the right opportunity to strike and then exit as soon as possible to minimize market risk. Hence, he will will buy stocks and then sell off once he made some money. I argued with him that such approach is akin to "Trading" and is extremely risky. But the funny thing is, he quoted a few examples which silenced me totally and seems that he is in fact doing a lot better than me in terms of returns on investments. Also, this will only work in US stock market and not our local SGX. Let me provide more details of what he argued upon.

2. Invest in US Stock Market- Singapore SGX is Dead?

The one thing super unique in the US stock market is that it swings wildly. Let me quote an example: Sentage Holdings (Financial Service Provider) IPO on Nasdaq. Its IPO price is US$5 per share but on debut day, it roared to US$52 (10 times) at one time but then after a while dropped down to US$4.60. The daily fluctuation can also be absurd. So you get the idea on how different US stock market is from our local SGX (dearth of growth stocks with business that has the potential to grow exponentially)

In the recent China Big Brother crack down on Didi Chuxing, my old buddy told me he bought into it and asked me to also do it. I looked at Didi Chuxing current conditions and politely told him I will not be investing into it due to home-based regulatory woes as well as that Didi Chuxing also just turned a profit recently (previously all losses). Turns out he had the last laugh as he mentioned that he made a cool US$30K in just a few days (this is more than what I earned in 1 year for my pathetic dividend income)-bought10 lots at US$7.50 and sold it when market got wind of news that Didi maybe looking into privatization and it went up to US$10.50 per share.

To sum it up, my buddy told me he spread his money on various US stocks and as long as 1 of them happens to be an outperformer, it would cover the losses (if any) from the others.

Summary

I think a lot of folks have made a lot of returns such as from holding Tesla which has increased in value 6 times over since 1.5 years ago. So US market seems to be filled with more potential growth businesses than our local SGX which is mainly made up of the old industries. But as for my buddy's investment philosophy, I am not sure what to make out of it. I called it luck but he called it his set of unique investment skillset. To each his own I guess as long as one makes money.