United Hampshire US REIT ("UHREIT") delivered another set of stellar results for its 2nd half FY2022. Looks like my greatest worries over the past few weeks over potential bad news being hidden by its management are unfounded. On the contrary, its operations have been vastly strengthen with refinancing of expiring major bank loans being successfully renewed till year 2026 as well as newly executed tenant lease renewal. In addition, 81.4% of its debts are fixed which will safe-guard UHREIT for possible further rate hikes by the US Federal Reserve which so far only has limited success to tame inflation. Key points to highlight here:

1. Improvement in Revenue and Net Property Income

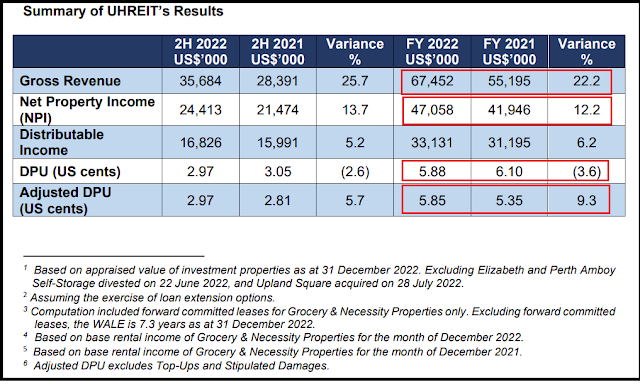

Gross Revenue and Net Property Income increases significantly by 22.2% and 12.2% respectively relative to 2021 due to largely due to the contributions from (i) Colonial Square and Penrose Plaza which were acquired in November 2021 as well as (ii) Upland Square which was acquired in July 2022.

Gross Revenue and Net Property Income increases significantly by 22.2% and 12.2% respectively relative to 2021 due to largely due to the contributions from (i) Colonial Square and Penrose Plaza which were acquired in November 2021 as well as (ii) Upland Square which was acquired in July 2022.

There were also improved rent performance of UHREIT Self-Storage properties that give rise to the better overall financials.

UHREIT has pointed to factors such as distribution income top-ups in previous years to explain the fall in DPU of <3.6%>. However, if one were to normalise this, the adjusted DPU would actually be 9.3% higher. Based on current DPU and recent closed price of US$0.520 per unit, this would still give an astounding distribution yield of 11.3%.

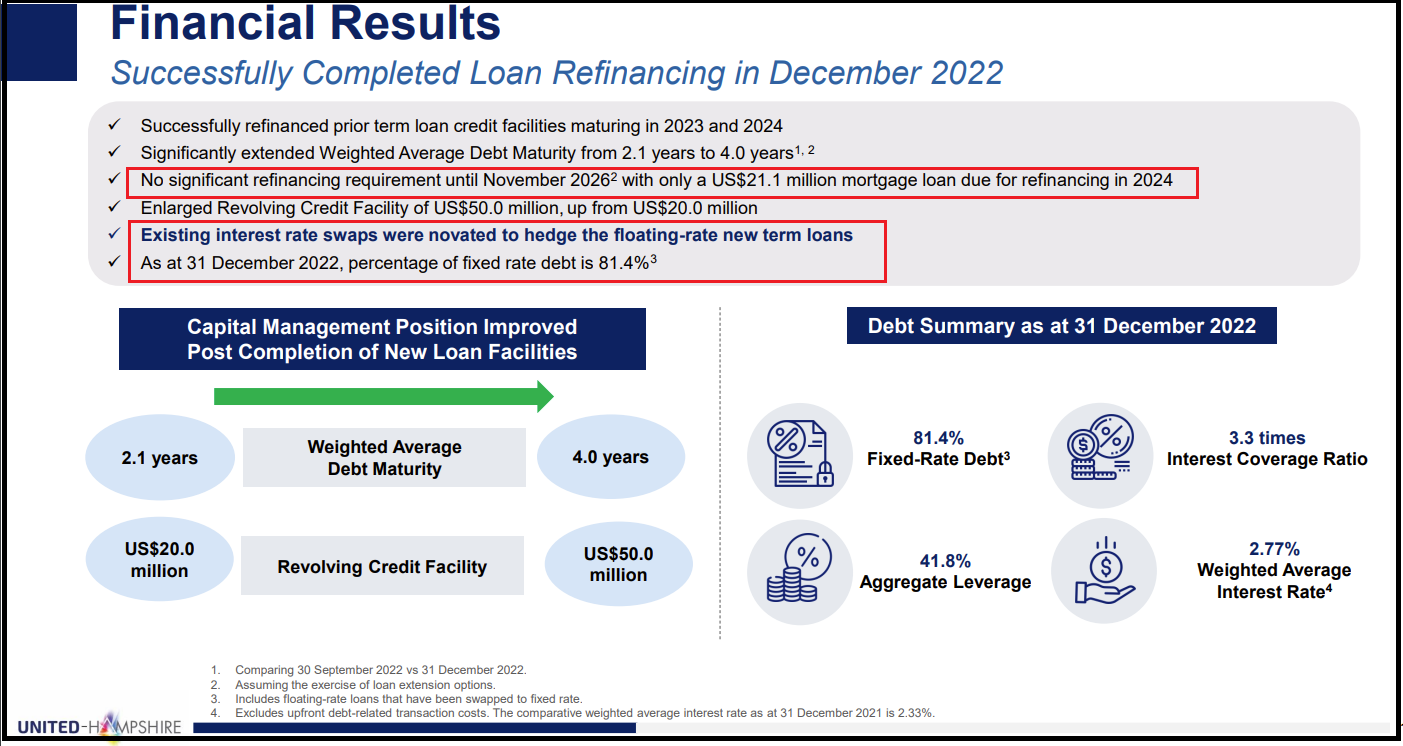

2. Credit facilities due in 2023 and 2024 were successfully renewed by UHREIT Management

UHREIT Management has successfully completed the bank credit facilities renewal in December 2022. There will not be any significant due debts (except for a small US$21.1Mil of loan due for refinancing in 2024) until November 2026.

3. UHREIT property valuation is one of the few REITs to have gone up slightly whereas most like Manulife US REIT have declined and has a NAV of US$0.75 per unit.

UHREIT announced that its investment properties valuation has gone up by 1.3% for 2022 which is impressive given the increase in termination capitalization rate for discounting purpose of future cashflow. Many REITs such as Manulife US REIT on the other hand experienced a sharp dive in their valuation. Do note that the positive valuation exclude Elizabeth and Perth Amboy Self-Storage divested on 22 June 2022, and Upland Square acquired on 28 July 2022, in case one is wondering why the published Income Statement shows a negative fair valuation gain in direct contradiction to the assertion in the press release.

Another interesting point is that the NAV of UHREIT is at US$0.75 per unit while its market price last traded on SGX as at 24 Feb 2023 is languishing at US$0.52 per unit.

Parting thoughts

Given the huge gap in terms of its NAV of US$0.75 per unit on top of a ridiculously high distribution yield of 11.3%, its current market price of US$0.52 per unit as at 24 February 2023 seems to be grossly undervaluing UHREIT from my personal view. I think that UHREIT management has done an excellent job so far. Most likely, I will be taking part in the distribution re-investment plan ("DRP") this round. Please take note of the final election deadline of 20 March 2023 if you are joining in the DRP.

Will you be taking part in the DRP? Do also share your thoughts and comments such as potential red flags that I missed with regard to UHREIT latest results that were released.