It has been painful to watch one of the most well known and iconic blue chip fall from grace. ComfortDelgro was once trading at S$2.80 per share during the pre-COVID lockdown days of 2019. It has since languished to S$1.13 per share as at 19 January 2023 which is a colossal decline of 59.6%. In 2018, I still recalled purchasing ComfortDelgro slightly below S$2 during the then recent market low point and then selling off when its price recover a little a few months later- I am just glad that I did not hold it long term otherwise I will now be staring at a huge capital loss. The key question that everyone is wondering seems to be at S$1.20 per share as at 10 February 2023, is comfortDelgro finally a good buy after coming off the trough of 52 weeks all time low of S$1.13 per share in January 2023?

1. View by some investors that Taxi business facing strong competition from GRAB hence leading to huge decline in ComfortDelgro revenue and profits.

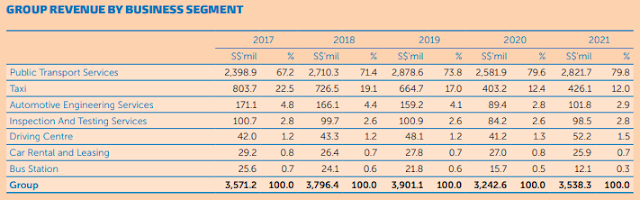

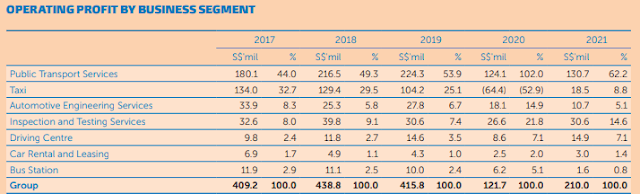

First and foremost, we need to address this strange perception by certain retail investors that the entire ComfortDelgro's share price is being punished due to poor performance of its taxi business against GRAB competition. From 2021 annual report extraction of Group Business Segment revenue, the taxi business consists only 12% of total consolidated revenue. If we look at operating profit level in 2021, the taxi business only contributed 8.8% of total group operating profit which is a remarkable turnaround from the lockdown 2020 of operating losses. With the worldwide lockdown (including China) coming to an end, there will be a gradual recovery from tourists coming to Singapore which should give a much needed boost to Public Transport as well as the Taxi segments in 2023- this is evident already in the 1st half results for 2022 and I think even more so for the results of 2nd half of 2022 that is yet to be announced. Overall, I do not think that GRAB still poses a major threat, they are in fact struggling to raise fresh capital in the current high interest rate environment and the era of using cheap financing to fund losses for marketing and market share expansion is over.

|

| 2021 Extract of Segment Results |

Another point to note is that even if we were to go back to pre-COVID days, 2018 annual report extraction of Group Business Segment revenue, the taxi business consists only 19% of total consolidated revenue. For 2018 operating profit level, the taxi business contributed a significant 29% of total group operating profit which in terms of quantum is around a S$100Mil differences to 2021 due mainly to a double whammy of a decline in revenue generation from lesser demand and a substantial increase in operating costs.

|

| 2018 Extract of Segment Results |

|

| Trending of Segment Revenue 2017 to 2021 |

|

| Trending of Segment Operating Profit 2017 to 2021 |

Using a hasty mental projection, pre-COVID period price range at end of 2021 and mid 2022 is around S$2.42 per share on average while operating profit has dropped by around 50%. So S$1.21 per share seems to be a reasonable hair cut that has some additional upsides like further recovery in transport demand built in.

2. PE ratio 17.46 using 5 years historical data.

From earnings of S$0.0548 per share during the 1st half of 2022, annualised impact is S$0.1096 per share. This gives a projected future price of S$1.90 per share based on historical PE ratio.

From earnings of S$0.0548 per share during the 1st half of 2022, annualised impact is S$0.1096 per share. This gives a projected future price of S$1.90 per share based on historical PE ratio.

Parting thoughts

Personally, I have started initiating bite size positions into ComfortDelGro at prices of S$1.19 per share to S$1.20 per share as I think that the worst is over for ComfortDelGro. The dividend yield (as per StockCafe) is around 5.3%. Perhaps more importantly, I need to diversify my dividend portfolio away from holding on to more REITs.

Hi Blade Knight, interesting that Comfort Delgro has been a hot topic lately. I previously bought in at 1.43 cost basis when it was August last year but quickly sold as I realised I did not have the sufficient conviction to hold through. My initial investment thesis was actually a rather simplistic one, based purely on the fact that I realise Grab was becoming more expensive than Comfort, even though they were barely profitable. Hence, I was convinced that Grab would eventually fade out of prominence and ComfortDelgro would regain its place as the private transport king of Singapore. Based off some quick glances, I suspect that the recent decline in share price is mostly due to the potential loss of some bus routes, and not merely based on the present earnings of the company. Additionally, I feel that perhaps basing upside off historic PE ratio may be slightly optimistic as I feel that the overall transport business has been receiving a large influx of new competition, coupled with lowering driver supply which would drive up labour costs. This could lower margins drastically. Nevertheless, I still do think Comfort Delgro has some decent upside, so I hope some profits materialise for you!

ReplyDeleteHi King, thanks for dropping by and sharing your thoughts....much appreciated. Yup, the potential loss of 1 or 2 of the bus routes is another issue here facing ComfortDelgro. I do hope that it is priced in already else there will be another plunge coming for ComfortDelgro.

ReplyDeleteThe current Operating Margin for taxi is already at an all time low coming off the huge loss from FY2020 and internal restructuring. I also shared your concern on the short supply of drivers as recently, I noticed that it is extremely hard to get a GRAB or taxi. In such instance, most probably the price of private car/taxi services will need to further increase in order to reach an equilibrium macro point between demand and supply.

ComfortDelgro ("CDG") is actually one of the very boring old school business providing traditional transport services as its main principal activity. Apparently, I do not have much affinity with CDG as my past investments often did not make much.

Saying that, at such low price amidst a recovering transport sector from post covid-lockdowns, I do hope that the dividend yield of at least 5%+ can be maintained for the long term.