On 13th February 2023, Lippo Malls Indonesia Retail Trust ("LMIRT") management announced that Moody's Investors Service has downgraded the corporate family rating of LMIRT and the senior unsecured bond issued by LMIRT to Caa1 from B3. There is unease in the whole market that LMIRT has no workable refinancing plans for its bank loan maturing in November 2023 and January 2024 and also its US dollar bond that will mature in June 2024 amid the high interest rate environment and risk conscious bankers. Not forgetting what happened during the recent COVID crisis to First REIT (another Lippo Group related REIT listed on SGX), it seems that another group of retail investors is on the verge of falling victim to the poor management by the Lippo group. 3 things to take note of with regard to LMIRT albeit the seemingly very attractive distribution yield of 11.6% per annum:

1. Falling Indonesia rupiah strength relative to SGD and worsening property valuation double whammy on top of expiring banking facilities

LMIRT is not just facing refinancing risk of a whopping S$400Mil in bank loans and bonds due over coming 12-18mths but also a continuous weakening of Indonesian rupiah against the Singapore dollars. Its leverage ratio is already at 42.2% as at 30 September 2022. There is a real risk of LMIRT breaching its bank loan covenants if valuation worsens.

There is only S$106.7Mil of cash and cash equivalents on hand on the balance sheet of LMIRT as at 30 September 2022.

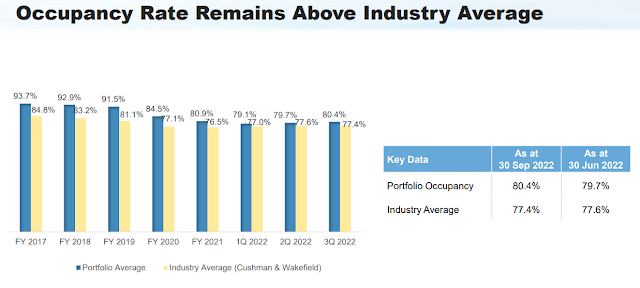

2. Occupancy rate above industry average is just an illusion- its mall only has 80.4% occupancy rate and worse still, a significant part of tenants are related to the Lippo Group.

|

| Occupancy rate above industry average? |

3. Lippo Group has a long track record of throwing retail investors under the bus.

I will not waste time here to write about what happened to OUE Commercial REIT (you can google it to find out more on the non-yield accretive M&A deal in 2018 on OUE Downtown acquisition and the rights issue impact on retail investors).

For First REIT, I have written many posts previously on how retail investors were being short-changed and the massive destruction of value.

Parting thoughts

There are various key reasons (as discussed above) on why the REIT has dropped from S$0.392 per unit to the current S$0.031 per unit and trading at 60% discount to its NAV over the last 5 years. Personally, I have seen how the Riady family run their business and took advantage of retail investors-look at how First REIT is being run to the ground with their reneging of original master lease agreement and also value destructing super lowly priced rights issue to save their own skin while throwing everyone else under the bus. I will not be surprised that Lippo will do another one onto LMIRT. So personally, I am keeping a ten foot pole away from any businesses setup by the prominent Lippo Group and the Raidy family.

No comments:

Post a Comment