Digicore REIT is one of the worst performing SREITs over the past 1 year. From its peak of US$1.20 per unit during Jan 2022, its unit price dropped to US$0.50 as at 31 October 2022. This is a shocking plunge of <58%> of its market valuation, all in less than 1 year. If one had subscribed to its IPO in December 2021 at US$0.88 per unit, the loss would still have been a mind-boggling <43%> decline in original investment cost. Current market price of Digicore REIT is languishing between US$0.50 to US$0.60 per unit. As at 22 November 2022, its unit price of S$0.555 means that it is at an annualised distribution yield of 7.42% which is way higher than what Mapletree Industrial Trust (6% yield) and Keppel DC REIT (5.6% yield) are offering. In addition, its future distribution is expected to grow 2% with the upcoming partial acquisition of Frankfurt data centre. So whatever happened to Digicore REIT for the market to punish it so severely? Is Digicore REIT a starbuy currently or is it a dividend value trap?

1. Investors are very worried that the Tech Industry woes will spill over to Data Centres.

The main concern for investors seems to be that the current crisis faced by the Tech Industry will lead to many default in rental as well as lowered demand for data centres. It probably does not help that Digicore REIT had earlier announced that one of its major tenants, Sungard Availability Services, had filed for bankruptcy protection.

In response to questions from unitholders, Digicore REIT disclosed on 17 November 2022 that it has reached an agreement with Sungard to amend the lease to allow for an orderly exit of the premises by 31 December 2022.

Digicore REIT also have in hand a surety bond or essentially a security deposit for two months rent. Moreover, the space in question is only 37,000 sqft and the REIT is confident of backfilling this space quickly.

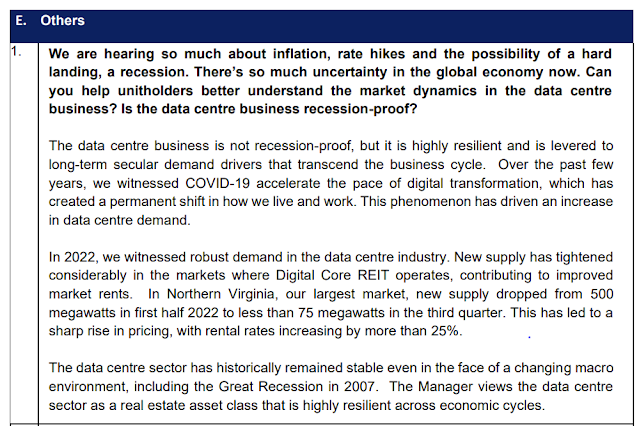

2. Interesting potential upsides of 25% increase in rental rate due to high demand for data centres and low supply.

Parting thoughts

Personally, I think that Digicore REIT is a starbuy at the incredulous 7.4% distribution yield on offer given the market expectation of an eventual 5% terminal borrowing rates by the US Federal Reserve. The huge decline in its price does offer one a relatively safer margin of error and to wait out the catch up in its market valuation. I reckon that a 20% increase in future market valuation is certainly possible and will collect the high distribution yield while waiting. I have slowly been accumulating additional units of Digicore REIT during this down period. Saying that, I plan to keep my investment cost in Digicore REIT to less than S$50K.

No comments:

Post a Comment