Why Do Some Investors Use Net Asset Per Unit To State That APTT Is Undervalued hence keep buying non-stop?

I would also like to add on that using purely Net Asset per unit to value APTT is not a good yardstick which some investors had relied on. This is because a huge chunk of the "asset" is tied up with an intangible asset in the form of a license to operate its business in Taiwan. The valuation of an intangible asset is fraught with lots of subjectivity depending on your beliefs. For my own sensitivity analysis, I would have impaired and discounted it severely based on the ever-weakening future cash flow generation from the entire business.

Is The Worst Over For APTT?

The million dollar question that everyone keeps asking now is whether the worst is over. Most importantly, is it a good time to buy undervalued units for APTT and also whether it is still a good business to invest in?

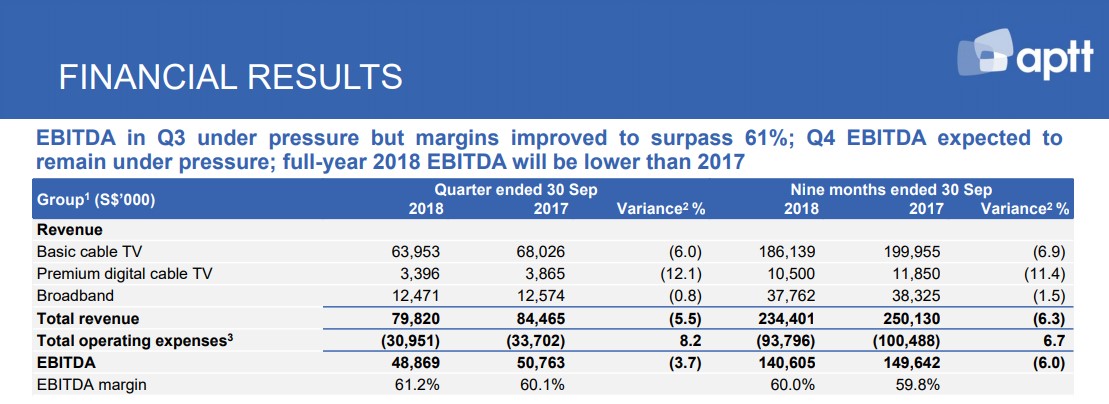

First and foremost, my personal view is that APTT has been massively oversold. There are no significant changes in the current business environment. The results show 9mths ended 30 September 2018 revenue declining by <6.3%> and EBITDA decreasing by <6%> whereas unit prices had plunged by 50%. I think that the fair value should be a lot higher. Also, the dividend payout after the cut is actually more sustainable. For those who dare goes in now will definitely have a higher probability of making profits. Generally, it is the entry price relative to the fair value of any type of business that determines whether the investment will turn out to be profitable.

Also, the extremely low price is actually making it an attractive offer for buy-out by existing shareholders such as Terry Gou (Hon Hai Group Chairman) or other big corporations.

Also, the extremely low price is actually making it an attractive offer for buy-out by existing shareholders such as Terry Gou (Hon Hai Group Chairman) or other big corporations.

BUT personally, I need to point out that while the unit prices are currently undervalued, there are unstable elements that are shaking the fundamentals of APTT and one may not be able to sleep well at night holding on to this counter.

3 Reasons Why Low Risk Tolerance Investor Should Stay FAR Far Away From APTT:

(1) Intense Competition from Pirates and Mobile unlimited Data Plans from Taiwanese Telecoms.

Consumers today are buying lots of TV boxes with free pirated TV shows. OTT such as Netflix, Viu, Youtube Premium etc are rising in popularity. Pay TV services is a declining market. For fibre broadband, they are also facing intense competition from Taiwanese Telecom companies which are offering unlimited Data Plans on the mobile network for connection. While the services are not obsolete, the revenue APTT can generate will continue to decline gradually due to a change in consumer demand.

Consumers today are buying lots of TV boxes with free pirated TV shows. OTT such as Netflix, Viu, Youtube Premium etc are rising in popularity. Pay TV services is a declining market. For fibre broadband, they are also facing intense competition from Taiwanese Telecom companies which are offering unlimited Data Plans on the mobile network for connection. While the services are not obsolete, the revenue APTT can generate will continue to decline gradually due to a change in consumer demand.

(2) APTT Management Team is either exhibiting excessive optimism from previously announced results or they are unsure of their own business and industry outlook.

I have previously pointed out in my other posts that the management keeps repeating that the ARPU decline is stabilizing. Apparently, their perception and definition of stabilization are very different from my own definition. Quarter by quarter it has been declining. I do not see anything stabilising about that aspect.

|

| Extract from previous QFY2018 Q2 Results Presentation |

In addition, during the 2nd quarter announcement, the APTT management team mentioned that they believed the unit prices are undervalued and that they are contemplating a share-buy back. But for the recent 3rd quarter announcement, it turns out that they have cashflow issue to fund future CAPEX without incurring more debts. Hence why talk about share-buy back when they do not even have sufficient funds to maintain the previous dividends and future CAPEX? I personally find such presentation contradictory to the ground situation and have sold off all my APTT units immediately after my last post in September'18 and hence was lucky to have avoided the recent crash in the unit price.

I hope that the major institutional investors will demand for at least 1 new senior management personnel to join the current APTT management team. It is time to do a global search or look in Taiwan for someone who can effect change by bringing in new perspective to the current business. Look at Starhub Singapore, it has done well with a new CEO who has brilliantly executed a cost-cutting exercise and a joint venture for cybersecurity.

I hold a view that a solid management team is a core to sustaining and developing a business and to continue to make it relevant.

I hold a view that a solid management team is a core to sustaining and developing a business and to continue to make it relevant.

(3) Massive Debts and Rising Interest Rate Environment

S$1.4 billion debt is actually a high risk to APTT as alluded to Reason 1 above. The old perception by everybody that APTT is a defensive stock and has stable cashfllow is actually no longer valid due to the declining customer demand. Banks are known to be fair weather friends. Once the marco economic environment sours or there are further decline in operating results that lead to banker's re-assessment, there is no guarantee in the loan agreements that the bankers are obligated to continue extending the borrowings indefinitely. The billion dollar debt is not a small amount.

I am also not confident that APTT will be able to get a lower financing charge upon renewal in the face of a rising interest environment and also declining business albeit gradually, that leads to worsening risk profile. Again, I do not share the same excessive optimism of the management team of APTT. Leverage is always a double-edged sword that cuts both ways.

Parting Thoughts

The current price of S$0.167 per unit includes dividend declared. Stripped off the Q3 dividend of S$0.016 per unit and ex-dividend effect will be S$ 0.151 per unit. From the revised dividends projection of S$0.012 per unit for FY2019 and FY2020, the dividend yield thus becomes 7.95% which is fairly decent as historical excessive dividends payout will be re-deployed back into the business as CAPEX investment.

The current price of S$0.167 per unit includes dividend declared. Stripped off the Q3 dividend of S$0.016 per unit and ex-dividend effect will be S$ 0.151 per unit. From the revised dividends projection of S$0.012 per unit for FY2019 and FY2020, the dividend yield thus becomes 7.95% which is fairly decent as historical excessive dividends payout will be re-deployed back into the business as CAPEX investment.

For more conservative and low-risk tolerance investors, it may be better to give APTT a miss in order to sleep better at night.

I am also not confident that APTT will be able to get a lower financing charge upon renewal in the face of a rising interest environment and also declining business albeit gradually, that leads to worsening risk profile. Again, I do not share the same excessive optimism of the management team of APTT. Leverage is always a double-edged sword that cuts both ways.

Parting Thoughts

For more conservative and low-risk tolerance investors, it may be better to give APTT a miss in order to sleep better at night.

Great post. I am not vested although had looked and considered before.

ReplyDeleteWho's that person with 300k shares? I wanna have a good laugh.

ReplyDelete