Singtel just announced its first-half results ended 30 September 2018. I actually think that it is a fairly good results being announced considering the intense competition faced by its overseas associate companies and Optus. Operating revenue surprisingly remained resilient and even grow 3% to S$8.4 billion. Margin eroded by over 21% (after normalisation from one-off gain from disposal of Netlink Trust in the previous year) mainly due to lower contributions from Airtel and Telkomsel as well as foreign currency translation losses from the effects of stronger Sing dollars against other currencies.

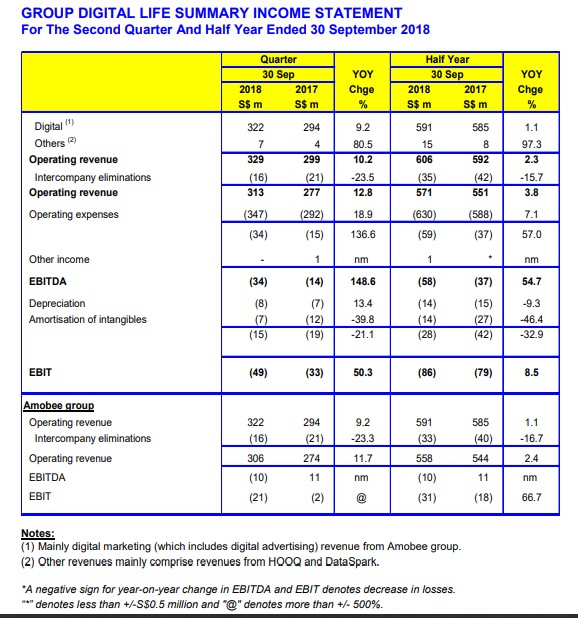

The only concern I have is that Singtel still has not stemmed the bleeding from Group Digital Life business. It continued with a widening of losses of <S$84Mil> based on the first half results. While I understand the importance of investing in this business segment which management seems to believe that there are perceived synergy to exploit on the Group's service offerings, the results have been depressing for years. They just can't seem to breakeven despite growth in revenue.

I have previously disposed all my Singtel stocks at prices of S$3.78 level as I do not like the intense competition with TPG jumping into the Singapore market by year-end. With the sharp decline in the prices of Singtel and which I think have been oversold, I have been accumulating new Singtel shares at prices ranging from S$3.060 to S$3.180 recently. The current business model from telecom business is still relevant and Singtel has proven to be defensive in nature over these past few months with lesser trading volatility relative to other blue chips.

An interim dividend of S$0.068 per share has been declared which represented a 2.19% yield based on the last traded price of S$3.10 per share and in line with expectation. Hence Singtel is still on track for its dividend guidance over the next 2 years of S$0.175 per share. This represents an annual yield of 5.65% which is fairly attractive while waiting for the share price to recover.

Hi, I started taking a look at Singtel last year. I stopped looking when I came across Amobee. This business is part of its Digital division I think? In my opinion, the whole division is loss making. We may give it time for the businesses to grow and bear fruit but if I am not wrong, Amobee has been around for around 5 years? Success stories in tech companies in the US like Amazon, Facebook etc are actually a dime in a dozen. Due to these stories and the impressions they generate, we tend to place a premium in pricing these entities. For me, I think the best course of action for Singtel (to put it bluntly) is to find the greater fool to take Amobee off its hands and maybe the other businesses of the Digital division along with it. At least, they will be able to stop the bleeding and maybe leave some useful spare cash for its telco businesses or as dividends. My general views, hope it can be useful.

ReplyDelete