Prime US REIT IPO ("PREIT") debuted on SGX on 19 July 2019 at a price of USD0.88 per unit. PREIT is sponsored by KBS Asia Partners which is one of the largest US commercial real estate managers with USD 28.3 billion under their direct investment and management belt. At one point in time, its market price even hit USD 1.050 per unit in the early part of 2020. Unfortunately, we all know what happened next. The March'20 stock market crash came along due to COVID lockdowns almost everywhere. PREIT share price struggled to break the USD0.80 per unit resistance level until recently. This was surprising given that its earnings has remained resilient during the COVID pandemic due to its excellent property Grade A portfolio, long WALE and good quality tenants.

1. Evaluation of Operations and Financial results Released For 2nd Half 2020 And Full Year.

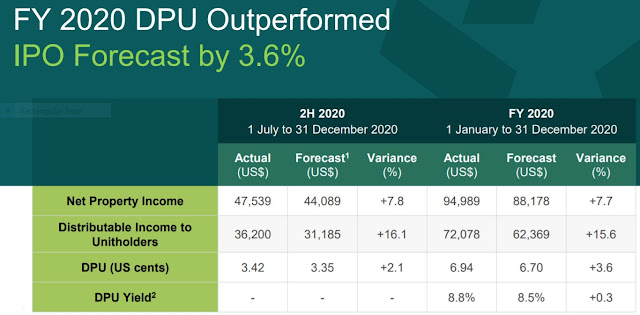

PREIT outperformed Net Property income IPO forecast by +7.7% and DPU also exceeded IPO forecast by +3.6%. This is a remarkable achievement in the face of the COVID pandemic.

225,222 sqft of space was renewed with positive rental reversion of 7.2%. Also 2021 48,603sqft of space was renewed with positive rental reversion of 6.9% which is an excellent start.

Properties are diversified sufficiently with no property contributing individually more than 15% to Net Property income.

99% of rent was collected and there were minimal deferrals throughout FY2020. Hence only a tiny amount of expected credit loss was provided in the full year comprehensive income.

In addition, high occupancy of 92.4% by PREIT relative to market benchmark of 86.8% with long WALE of 4.4 years.

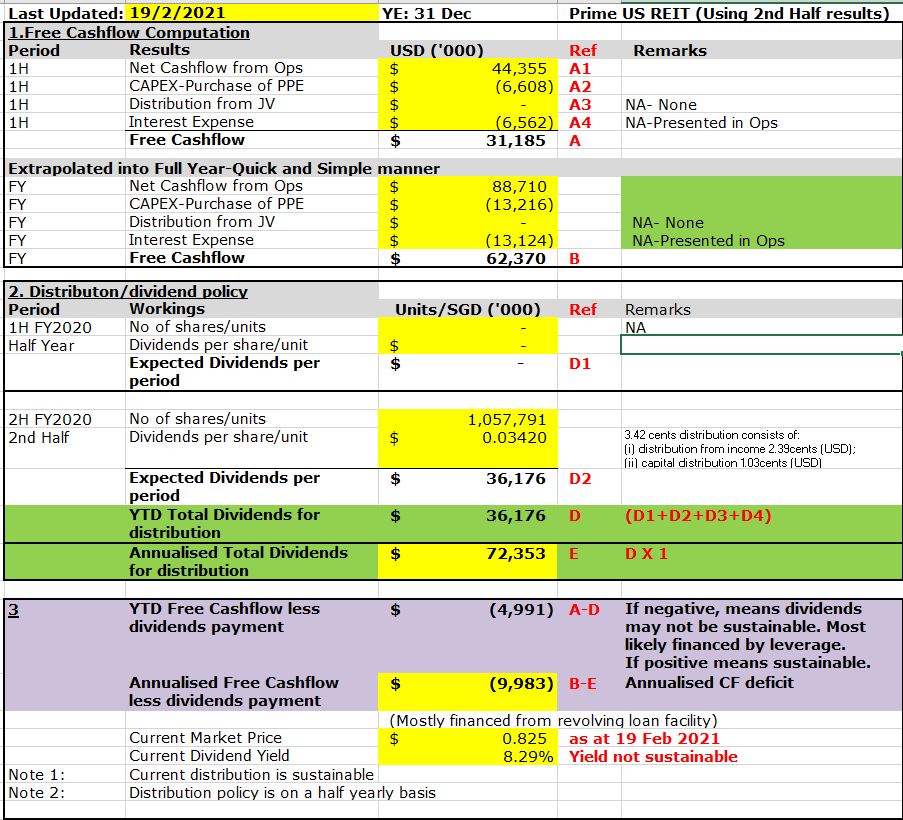

2. Free Cashflow and Payout Sustainability of PREIT

This is a complex issue. Many REITS have been using leverage to finance capital expenditure for investment properties including PREIT. Hence if this continues indefinitely, the gearing ratio may breach the MAS regulatory requirement unless the capital expenditure can enable PREIT to generate additional rental income in future.

Conserving cash and bringing down the dividend payout to a 7% yield instead of 8% maybe more prudent- personal opinion.

3. Quick comparison PREIT with Manulife US REIT.

1. Dividend sustainability- free cashflow analysis- please refer to point 2 above. Both REITs are similar in this aspect.

2. Manulife US REIT has relatively larger bad debt provision as at 31 Dec 2020. PREIT performed significantly better in terms of tenant credit management with 99% rental collected.

3. Due to the above, US Manulife US REIT cut DPU relative to prior year but PREIT increased their DPU relative to forecast.

4. PREIT has a relatively stronger balance sheet than Manulife US REIT. Its gearing ratio is at around 35% while Manulife US REIT is approximately 40%.

5. Personally, I think Manulife has a better branding locally than PREIT as it is more well known. An established name will ensure the REIT has a solid backer which cares about its reputation to ensure success and also easier on the relationship front to get funding from bankers during crunch time.

Summary

Overall, PREIT has performed exceptionally well for FY2020 despite the economic downturn caused by COVID. Let's hope the Biden administration does not come up with any changes in tax rules which may wreak havoc on the share price if withholding tax structure exemption for retail investors becomes an issue again.

Note: I am currently vested in both PREIT and Manulife US REIT .

No comments:

Post a Comment