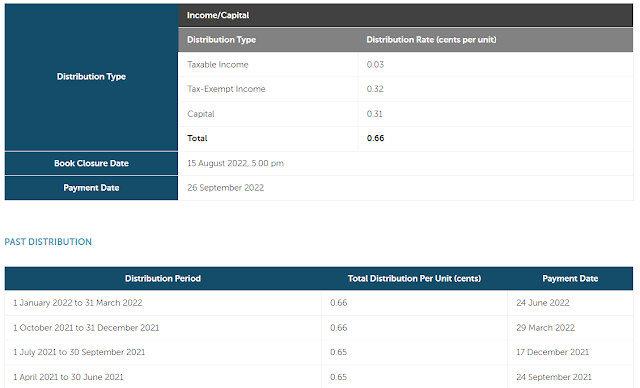

Recently, I was just wondering whether it is time to go back to holding a small stake in First REIT given the "2.0 Growth Strategy" implemented by its Manager to diversify concentration risk in Siloam hospital group in Indonesia. I thought that the 12 Japan nursing homes acquired in March 2022 was a good start for this new visionary strategic direction. The over-reliance on Lippo Karawaci's Siloam healthacare group has been nothing short of a disaster during the COVID crisis in Indonesia which led to a renegation of the original Master Lease Agreements (of course it was cleverly crafted as a "restructuring" of the master lease agreement) for 14 hospitals in Indonesia from 1st January 2021. Its last quarterly distribution was 0.66 cents per unit which when annualised gives an amount of S$0.0264 per year and an amazing annual +9.78% distribution yield at the closing price of S$0.270 per unit as at 26 August 2022.

1.High distribution yield of +9.78% per annum looks super attractive is it not?

2.Perpetual Unitholders which lent money to First REIT in 2016 got screwed by Management.

First REIT recently launched a tender offer to buy back S$60 million in Series 002 subordinated perpetual securities in cash, at only 70% of the original principal amount. My first thoughts were: "Like that also can for redemption of perpetual securities?"

The management of First Reit said that the rationale for its offer is to “provide liquidity to the securityholders given the illiquid nature of the outstanding securities”, and to optimize the trust’s debt capital structure as part of its continuing capital and liability management initiatives.

Again, First REIT looks set to take advantage of its investors by not redeeming back the bonds at its original issuance price. Perpetual security lenders of First REIT will find that they barely got back the entire capital ploughed in even if the interest rate was 5.68% per year in 2016. Future prospective investors of perpetual securities may ponder whether it is a wise move to invest with First REIT.

Parting thoughts

With an attractive annualized distribution yield of 9.78% and the forage into other healthcare properties other than Indonesia's Siloam hospitals, First REIT seems to be embarking on a new growth path that at the same time also aims to diversify its over-reliance on a single tenant as well as geographic segment. This is definitely a step in the right direction.

However, its recent sales of a hospital at only a slight premium plus redemption of perpetual securities at a fraction of the original principal amount does make one suspicious of whether First REIT is back to short-changing investors again notwithstanding the bad track record of "restructuring" of the Master Lease Agreements 2 years back to reduce the rental expenses of Sponsor's Siloam Group. In short, First REIT management's penchant to throw investors under the bus maybe a reason for the extremely high risk premium relative to the risk free rate. Hence I think I will still be staying away from First REIT for now.

Bad for perpetual, good for shareholders

ReplyDeleteHi Brandon, yes, if talking about the 70% for perpetual, this is good indeed for existing unit-holders. In spite of that, If we take a step back and look at the whole episode from a broader perspective, it still looks to me Management more interested to act towards sponsor's interest rather than all unit-holders and other investors- my own personal view point only. :)

Delete