Mapletree Industrial Trust ("MIT") has been battered down over the past 1 year. Its market price has dropped from S$2.93 per unit to a low trough of S$2.40 per unit in May 2022 which is a plunge of <18.1%> from a year ago. Its current market closing price of S$2.56 per unit as at 16 September 2022 probably gave scant comfort to retail investors who have bought into MIT during the past 2 years. Is it time to sell one's MIT in view of the ongoing relentless interest rate hikes by the US Federal Reserve that is pushing the entire global economies into a deep recession?

1. Fear mongering by "experts" and Media on REITs in trouble due to interest rate hike

First and foremost, the one thing that I really cannot stand is that I have been hearing a number of folks around me or online shouting out loud that interest rate hikes will lead to higher costs of borrowings hence now is not the time to be holding on to REITs. Hello? Many commercial businesses (and not just SREITs) borrow money to run their business. So a higher borrowing costs will hit not just REITs but most of all other businesses.

In addition, many properties in REITs being leased out have inflationary linked rental component. Even if not, upon lease renewal in an inflationary environment, REITs similar to other commercial businesses, has the right to ask for uprates in rental income which is different from debentures nature financial instrument. ESR-ARA Logos REIT and Mapletree Logistics Trust have "service rate" component in their overall rental package that is not tied down to the duration of the lease but allows the landlord to increase the service rates at their discretion in order to cover for common properties maintenance. Recently, I have seen some of the logistics REIT exercising such right in their warehouse tenancy agreements to push up the service rate component by over 17% this year.

So, please stop thinking that REITs are similar to bonds- both are entirely different creatures altogether.

|

| Past 1 year market price of MIT trending downward |

2. Recession fears increasing by the day and risk to MIT

Recession rather than higher borrowing rates due to interest rate hikes (as alluded to pt 1 above) should be more worrisome. Just recently, FedEx Corp sounded a profit warning due to a record plunge in package deliveries. If transport aren't moving, it signaled that the economy isn't moving much too and gave rise to an indication that the stock market will tank further should the macroeconomics situation worsen.

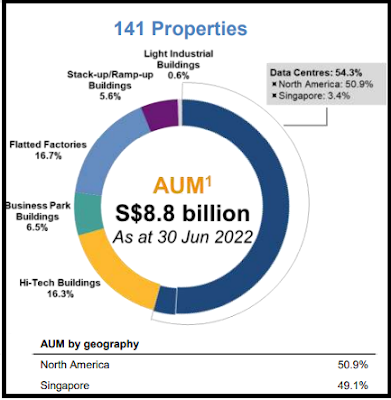

The risk of tenants of MIT going into bankruptcy and default should there be a severe recession is not unfounded. However, given the focus of MIT into high tech industrial sectors and also data centres, my personal belief (based on the experience of COVID-19 lockdown) is that the earnings of MIT are sufficiently resilient. 54.3% of MIT's asset under management are coming from Data Centres and 16.3% are into Hi-Tech Buildings segments.

Parting thoughts

For myself, I look at my MIT holdings in my investment portfolios (bought using cash and margin) with a long term horizon and is not perturbed by the wild swinging market movements. I am certainly very much amused by the so many experts or gurus that can predict the stock markets ups and downs and are advocating for selling down one's equity portfolio due to upcoming "recession" headwinds. Personally, my own experience is that staying almost fully invested allows one to take part in any possible corporate actions such and M&A rights issue or takeover from other companies. Most importantly, what if the stock market suddenly rallied? One would have missed such golden opportunity if one is too fixated on timing the market.

P.S: Just to sidetrack and to share my personal story regarding my CPF investments (this is not included in my published investment portfolios), I just sold off my CPF Ordinary Account investments of MIT (10,300 units held over 1.5yrs) @$2.62 per unit last Monday (12 September 2022) as I wanted to re-invest the funds into the S&P500 for greater returns in the longer run. But in a strange twist of fate, MIT's unit price suddenly dropped to S$2.54 per unit on Friday (16 September 2022) and I can't resist but buy back 10,000 units at this more favourable entry price. Yes, I strongly believe that MIT has a bright future ahead based on the well-executed strategic moves by the Mapletree senior management thus far.

No comments:

Post a Comment