Lendlease Global Commercial REIT ("LREIT") announced that it has acquired a 5% stake in JEM shopping mall in Jurong East. While the current acquisition stake is only 5%, it has demonstrated that LREIT has good potential for future growth due to the many properties that could be injected by their sponsor Lendlease Group. The diversification into a suburban mall with 12 levels of office further increases the resiliency of its future earnings. My personal thoughts are LREIT share price is severely undervalued and the market is putting up excessive risk premiums on LREIT relative to its peers.

1. LREIT Background

LREIT IPO price was at S$0.88 per unit on 2nd October 2019 (about 1 year ago). It later went up to S$0.955 per unit at one point in time before plummeting to an all time low of S$0.440 per unit during the March 2020 stock market crash. Holding on to Lendlease is thus a roller coaster ride despite the fact that it has two extremely good quality properties in its portfolio. LREIT derives around 66% of its property income from 313@Somerset and 34% from Sky Complex in Milan.

2. LREIT remains severely undervalued- COVID-19 will not last forever

LREIT happens to be severely undervalued at the current unit price of S$0.69 per unit as at 2nd October 2019. While there have been rental reliefs granted to tenants during this pandemic induced economic crisis, its fundamentals remain intact. You can go down to Orchard Road to take a look. The young and the beautiful are all flocking back to 313@ Somerset after the circuit breaker. Its Sky complex office portfolio also remained resilient due to the sheer financial strength of its tenant despite the terrible COVID-19 situation in Europe.

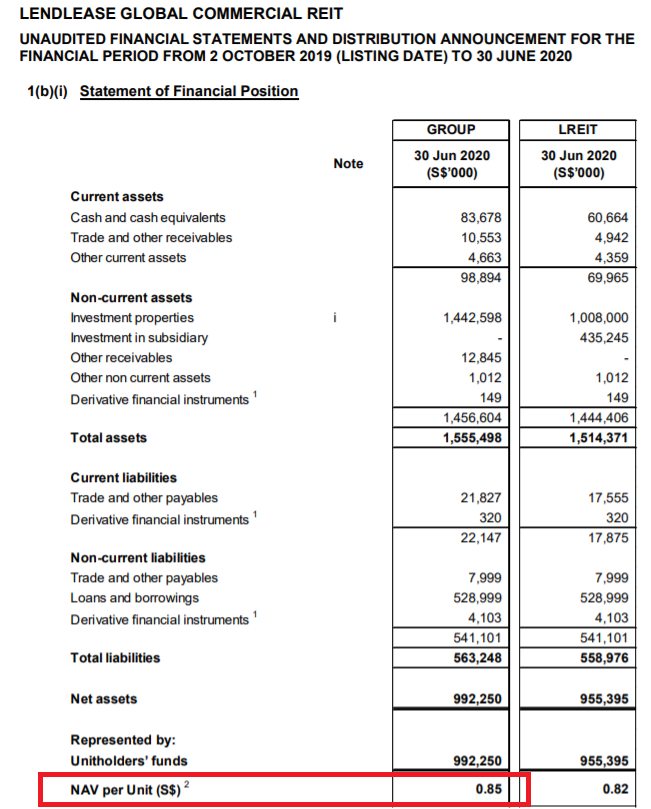

Net asset value as at 30 June 2020 is S$0.85 per unit. Current market price to book value is at a discount of 16%.

The IPO projection for FY2021 was initially 6% dividend yield. Current net profits for full financial year is down 20% from forecast due to the rental relief packages. Once the pandemic is over and the economy on track back to normal, investors who went in at today's pricing of S$0.69 per unit will be reaping a dividend yield of 7.6% dividend yield per annum and also a capital upside of close to +45% based on target price of S$1 per unit in another 2-3 years (it already hit close to S$1 before the COVID-19).

3. Growth of LREIT is assured with latest additional investment into JEM shopping mall

The growth path for LREIT has been re-affirmed with the recent acquisition of a 5% stake in GEM shopping centre at Jurong East. There are thus many potential pipelines for LREIT to grow besides relying on the organic growth of Sky Complex and 313 Somerset.

Summary

I think that the potential upside for LREIT out-weights the potential downside risk of another devastating economic lock down. I have also ploughed back the recent dividends received from LREIT into my investment portfolio. Keeping my fingers crossed that a safe and effective vaccine will soon be released to stop governments from locking down the global economies again.

(Note: Currently, I am vested in 135,000 units of LREIT.)

Assumptions based on life going back to normal in the next few years. While many experts have predicted many changes that happened may become permanent even after vaccines become available.

ReplyDeleteThanks for sharing. What are the changes that happened that may become permanent even after vaccines become available? The shift to online shopping?

Delete