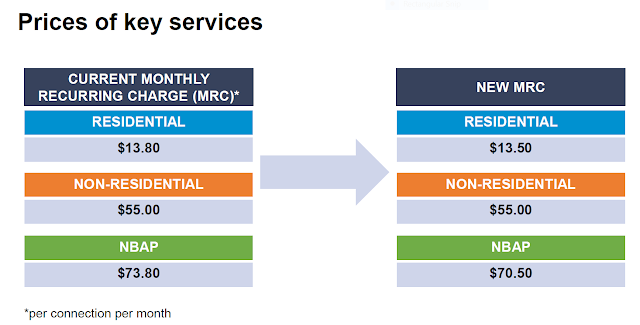

Netlink Trust ("NLT") announced on 27 November 2023 that the Infocomm Media Development Authority (“IMDA”) has completed their pricing review. I was shocked that the chargeable tariff has not increased at all despite inflationary pressures on labour costs, CAPEX and escalating financing charges. What was even more surprising was that the chargeable tariffs for Residential Connection and Non-Building Address Point got adjusted downwards (please click here for the YouTube Video version).

Basically, over the past 5 years, residential connections have grown from 1.2Mil to 1.5Mil which gives an compound annual growth rate ("CAGR") of 4.5% in terms of volume. Non-Building Address Points ("NBAP") has grown at an impressive 26.5%. Hence due to surge in volume economies of scale over total cost of operating the fibre network, this leads to a regulatory reduction in prices per connection.

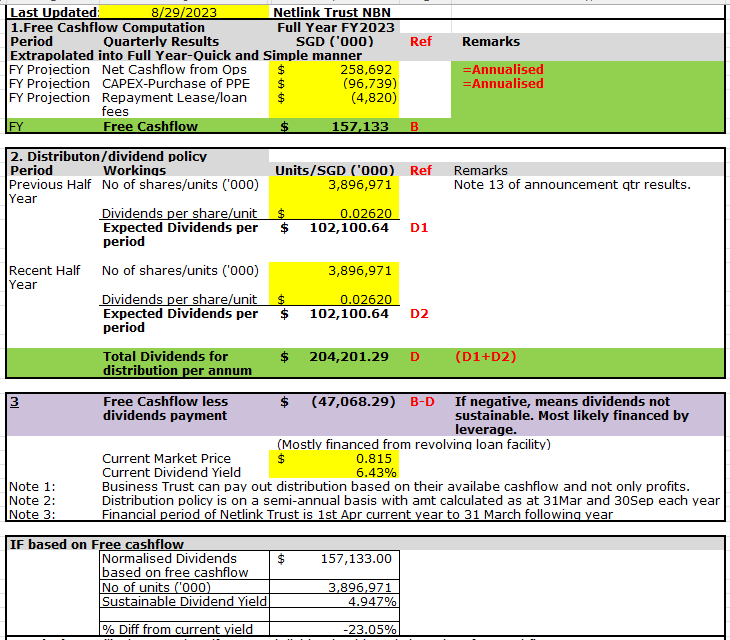

Distribution yield of 6.43% not sustainable over longer term

At the price of S$0.815 per unit, this represented a distribution yield of 6.43%. However, note that part of the distribution is being financed from bank borrowings which is not ideal. From a free cashflow perspective, the sustainable distribution yield will be at a lower 4.95%. Given that money market funds with online brokers hover around 4% to 5%, a mere 4.95% distribution yield from investing in NLT equity is beginning to look like a really bad choice.

Parting thoughts

As aforesaid mentioned, I am extremely disappointed by the outcome of the IMDA pricing review. If one is sure of the continued compound annual growth story of new connections in driving revenue, then NLT seems to be still a good investment. Personally, I will not be adding on to my stakes in NLT as I think that the IMDA wants the shareholders to do charity work and the borrowings to fund dividend distribution is a strange concept to me. Nevertheless, I will still be keeping my minor stake in NLT for now.

This hits me like a brick. I'm 1/4 into NLT.

ReplyDeleteHi Damn, how are you? Good to hear from you always.

DeleteThe revenue growth story probably will still be intact based on growing connections in future years. Just that personally, I think it is kind of absurd with a price reduction (at least keep it the same) when most business are increasing price of their products or services to keep ahead of the high inflationary environment.

Also the CAPEX for NLT business such as NBN 2.0 do worry me.

There is definitely some uncertainty in the business visibility where I am not sure whether the growth in connections revenue can continue to outweigh the operational costs components in future.

Ah Kong use his companies to do national service. GE coming ah. See Singtel & Starhub same fate.

ReplyDeleteHi Henry,

Deletehaha....GE coming indeed. :)

Lol i actually sold this earlier because of what you pointed in an earlier post on the substainability in Aug 2023.

ReplyDeletehttps://dividendpassiveincome.blogspot.com/2023/08/netlink-trust-61-distribution-yield-not_30.html?m=1

Hi YX, yup, the sustainability of the distribution is always an issue with NLT. I cannot comprehend their mgt team thoughts that since leverage ratio is very low, this is a good move to fund it with more borrowings.

DeleteNLT is like a shipping trust, example FSL.NAV keep depreciating every year, as investors receive dividend. Can't hold for long term.

ReplyDeleteReits, physical properties, at least there's a chance that it will increase in price if the property is good.

Fully agree....the fixed asset-heavy trusts have this unfortunate issue.

Delete